Wars, markets and economic growth

- 05.01.26

- Economy & Policy

- Commentary

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

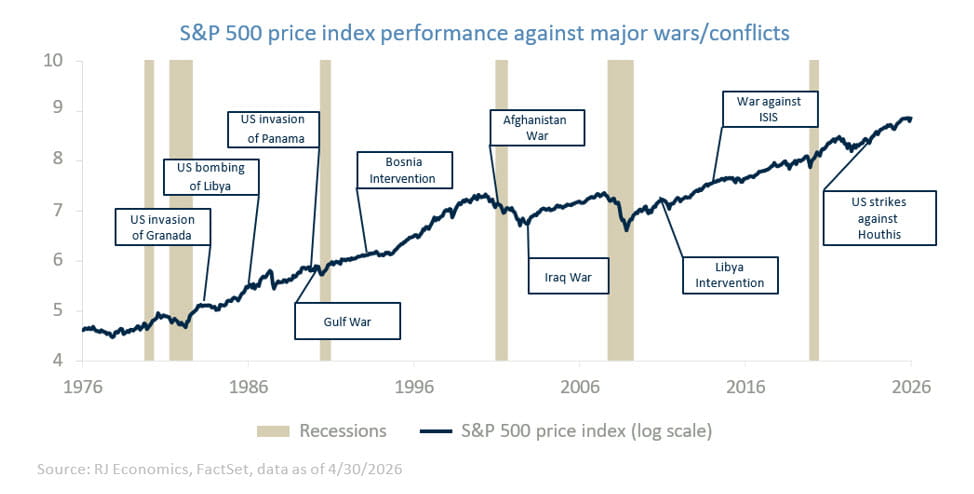

A few days ago, a client shared a chart produced by a think tank or a bank economics group that tracked the performance of the S&P 500 over the past five to six decades (recreated and expanded above). Superimposed on the index were markers identifying each major military conflict involving the United States during that period. The message of the chart was hard to miss.

Despite repeated wars, equity markets have delivered strong long-term returns, and in some stretches, market performance appears to have coincided with wartime episodes rather neatly. Viewed through the lens of financial markets, the implication seems almost intuitive: wars have not been bad for investors and may even have been supportive.

This idea is not new. Many of the textbooks used in undergraduate and graduate macroeconomics feature similar historical charts, showing notably strong economic performance during periods when the US was engaged in military conflicts. Students would naturally connect the dots and reach the conclusion that wars must be good for economic growth. From an investor’s perspective, the leap is even easier: if growth is stronger during wars, corporate earnings rise, markets respond and risk assets benefit.

The temptation to accept that conclusion is understandable, but it misses the underlying drivers that matter most for markets. The historical relationship between wars and asset prices does not reflect the intrinsic economic value of conflict. Instead, it reflects the way fiscal policy behaves during wartime and how that policy feeds directly into growth, earnings and risk appetite.

The first crucial distinction is that US wars over the past several decades have been fought almost entirely outside US territory. Capital stock, infrastructure and labor markets at home remain largely intact. From a macro and market standpoint, that means the economy experiences the stimulus of higher government spending without suffering the offsetting destruction that would normally accompany war. Had these conflicts damaged domestic productive capacity, the market narrative would look very different.

The second, and arguably more important, factor for investors is fiscal behavior. Wars effectively suspend normal budget constraints. Policymakers, regardless of party affiliation, tend to authorize large increases in spending with limited concern for deficits, debt dynamics or future financing costs. From a Keynesian* standpoint, this is a textbook growth impulse. From a market standpoint, it translates into higher nominal demand, stronger top line revenue growth for firms tied directly or indirectly to government outlays, and a broader lift to economic activity.

This dynamic remains relevant today. The economy is already operating with a big amount of fiscal support, even before accounting for additional military spending related to the war in Iran. That war represents incremental spending layered on top of the fiscal expansion embedded in the One Big Beautiful Bill Act. This is a central reason we have not revised our growth outlook lower this year, even as households are expected to funnel much of their higher tax refunds into higher gasoline and energy costs rather than discretionary spending.

From a market perspective, the fiscal impulse does not stop there. The government is also scheduled to return roughly $170 billion in tariffs to firms over the course of the year, adding another channel of support for cash flow, margins and investment spending. Taken together, these factors create an environment in which nominal growth remains resilient, earnings risks are cushioned, and downside scenarios for risk assets are delayed, even if underlying fundamentals appear more fragile beneath the surface.

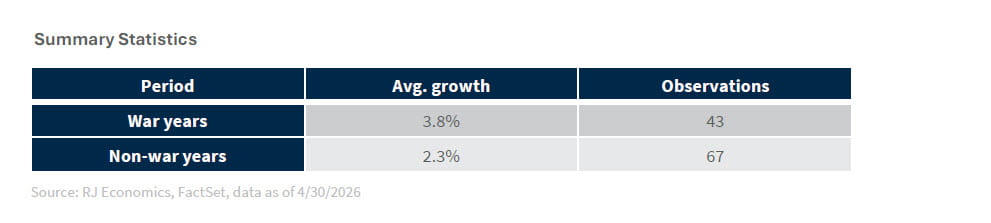

As a result, we arrive, somewhat uncomfortably, at the same conclusion that students and many investors reach when looking at historical data: Wars appear to be good for the US economy and for markets. The summary statistics reinforce this perception. Average growth during wartime has been higher than during non-war periods, and asset prices have tended to perform well alongside that growth. Markets respond to flows, demand, and earnings, not to philosophical debates about the social cost of conflict.

The deeper point, however, is that this outcome has far less to do with war itself and far more to do with the willingness of policymakers to spend aggressively. The US could, in principle, achieve similar growth and market outcomes by deploying comparable fiscal resources toward infrastructure, productivity enhancing investment or other domestic priorities. Wars are not growth positive because of what they destroy or defend, but because they justify spending on a scale that would otherwise be politically difficult.

For investors, the implication is both constructive and cautionary. As long as fiscal expansion persists, growth and earnings can remain supported, even in the face of higher energy prices, tighter monetary policy or weaker household balance sheets. But once the war effort winds down and fiscal impulse fades, the same forces that lifted growth and markets tend to reverse. Historically, economic momentum slows, earnings expectations reset and markets are left to reckon with the debts accumulated along the way.

In that sense, wartime economics often turns policymakers into short term Keynesians, while markets gladly price the upside. The longer-term implications, particularly for debt sustainability and future growth, are deferred until well after the immediate market narrative has played out.

*Keynesian economics is an economic school of thought based on British economist John Maynard Keynes, emphasizing that government intervention (fiscal and monetary policy) is necessary to stabilize the economy, particularly by boosting aggregate demand during recessions. It advocates active intervention to manage business cycles, such as deficit spending to reduce unemployment.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.